Table of Content

Home equity loans best suit borrowers who have a substantial amount of equity available to them. You can determine the total amount of equity in your home by subtracting any and all debts secured by your house from the current fair market value of your home. The amount left over is the total equity, or value of ownership, of your house.

So if you do a cash-out refinance, you can’t take out a home equity loan until the mortgage is paid off. Texas law caps home equity closing costs at 2% of the total loan amount. If you still owe money on your home, you’ll continue paying the same mortgage in addition to your home equity loan payments.

How much are home equity loan closing costs?

Cash-out refinancing is better suited for planned expenses, such as home renovations or paying for college tuition. If you want to create a safety net for unexpected financial burdens (say, for example, your roof springs a leak and you determine it’s in need of replacement), a home equity mortgage is your best option. Cash-out refinancing tends to come with a lower interest rate than home equity loans. While home equity loans have lower closing costs, they are typically more expensive over time due to higher interest.

VA loans are an exception, as they allow you to get a cash-out loan for 100% of the value of the home. When you do a cash-out refinance, you usually can’t get a loan for the entire value of the home. Many loan types require that you leave some equity in the home. As you repay your mortgage over time, the equity in your home will increase. But the homeowner now has a $100,000 in cash to use for however he wishes, without changing the rate or term of his existing first mortgage.

What You’ll Be Responsible for Repaying

It also depends on your income, credit score, and other financial factors. The difference in value between your home’s worth and your mortgage balance ($70,000) is your home equity. You could take out a home equity loan to access part of this $70,000 as a lump sum. Cierra Murry is an expert in banking, credit cards, investing, loans, mortgages, and real estate. Cash-out refinance is available through either a fixed-rate mortgage or an adjustable-rate mortgage. Your lender can provide information about fixed-rate and adjustable-rate mortgage options so you can decide which one best fits your situation.

If you fail to pay back your loan, the lender on your initial mortgage has the first claim to the property—not your home equity lender. Therefore, higher interest rates offer lenders added protection. A lender will determine how much cash you can receive with a cash-out refinance, based on bank standards, your property’s loan-to-value ratio, and your credit profile.

Do You Have To Pay Taxes on a Cash-Out Refinance?

You usually pay a higher interest rate or more points on a cash-out refinance mortgage, compared to a rate-and-term refinance, in which a mortgage amount stays the same. Cash-out refinances are first loans, while home equity loans are second loans. Cash-out refinances pay off your existing mortgage and give you a new one.

While we adhere to stricteditorial integrity, this post may contain references to products from our partners. The offers that appear on this site are from companies that compensate us. This compensation may impact how and where products appear on this site, including, for example, the order in which they may appear within the listing categories.

How To Flip A House And Get Started In Real Estate Investing

Also, a home equity loan really only makes sense if today’s interest rates are either the same as, or lower than, your current mortgage interest rate. Sarah Li Cain is a freelance personal finance, credit and real estate writer who works with Fintech startups and Fortune 500 financial services companies to educate consumers through her writing. She’s also a candidate for the Accredited Financial Counselor designation and the host of Beyond The Dollar, where she and her guests have deep and honest conversations on how money affects our well-being. Once you do a cash-out refinance, you then pay it back on monthly installments according to your loan terms. There are a few ways you can tap in your home equity, each with its own advantages and disadvantages.

The home is currently worth $500,000 and the homeowner has an existing mortgage balance of $300,000, so there is $200,000 in available home equity. There are 2 types of home equity debt – home equity loans and home equity lines of credit, also known as HELOCs. Whatever your reasons for accessing the equity in your home, it is critical to know the differences between these two loan options so you can choose the one best suited to you.

Also, if you are 20 years into a 30-year mortgage and every month you’re paying off more principal than interest, it probably doesn’t make sense to do a cash out refinance. It doesn’t make sense to do a cash out refinance if your new interest rate is higher than the interest rate on your current mortgage. It only makes sense if you are refinancing to a lower interest rate.

However, your loan amount is also contingent on other financial factors, like your income and credit history. This can increase your risk level and is not recommended unless you are certain you can make your mortgage payments on time every month. Your home’s equity will fluctuate based on how much repayment you’ve made toward your home loan and how the market affects your home’s value.

Depending on the housing market, a cash-out refinance may also give you access to better terms or a lower interest rate. Keep in mind that if you have a government-backed loan such as a VA, USDA, or FHA loan, you’ll most likely refinance to a conventional loan. As a general rule, you need at least 20% equity in your home to get a cash-out refinance. Most lenders won’t let you take out one of these loans if the loan-to-value ratio is above 80% . Since a refinance loan pays off the previous mortgage, it becomes the new first mortgage with the highest priority.

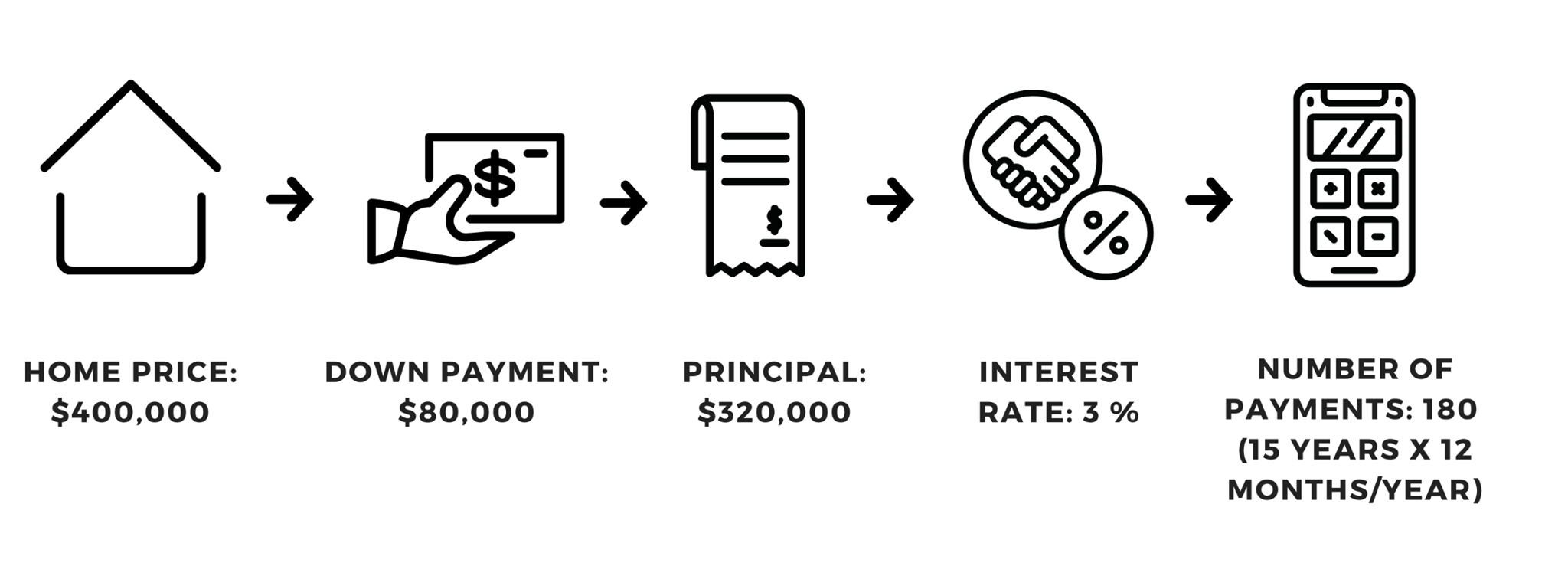

Since mortgages typically have lower interest rates than credit cards and auto loans, a cash-out refinance could save you a lot in interest over time. Generally speaking, home equity loans and HELOCs have shorter repayment terms than a primary mortgage. For example, most first mortgages are structured to be repaid over 30 years. However, home equity loans and lines of credit typically have repayment periods of 15 years or less . It is important to keep this mind because the shorter the repayment term, the higher your monthly payment will be. A home equity loan is a means of borrowing a lump sum using the equity you’ve paid into your home.

No comments:

Post a Comment